There are often benefits and drawbacks to having “full coverage” auto insurance, which typically combines liability, collision, and comprehensive coverage. This type of policy can cover costs for at-fault accidents and non-collision damage, within policy limits. It’s often worthwhile for high-value vehicles or when required by a lender, but some drivers may find only liability (required by most states) more cost-effective. Infinity Insurance Agency (IIA) can help you compare options so you can find the right fit.

When you buy a car, you may be asked to obtain full coverage insurance. But what is full coverage insurance? This is one of the most common questions drivers ask when comparing insurance options. Many people assume it is a specific type of policy, but the reality is a little more complex. In most cases, full coverage insurance refers to a combination of liability, collision, and comprehensive coverage that work together to provide broader financial protection in case of a covered accident.

While liability insurance helps cover injuries and property damage you cause to others, full coverage also helps pay for damage to your own vehicle from accidents, theft, vandalism, weather-related damage, and other covered events. Understanding what full coverage includes and where its limits exist can help you make informed decisions about your insurance needs.

Full coverage insurance defined

Many drivers hear the term "full coverage" and assume it means every possible situation is covered. However, full coverage is not a standalone insurance policy. Instead, it is a collection of coverages that typically includes:

- Liability insurance

- Collision insurance

- Comprehensive insurance

Together, these coverages provide broader protection than a minimum coverage policy.

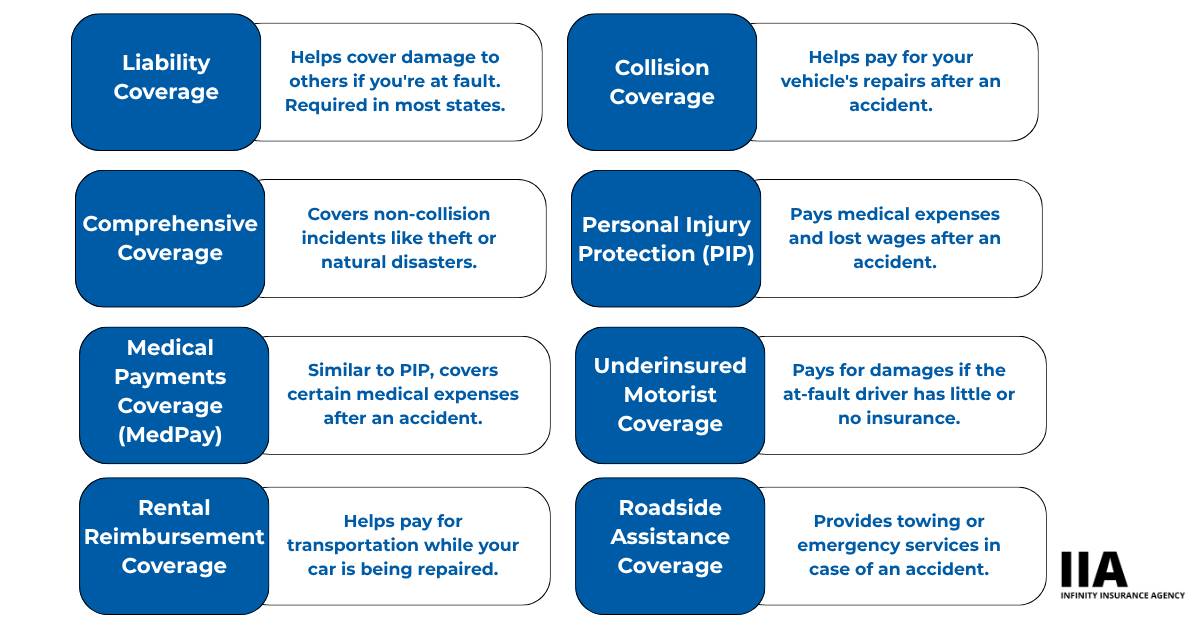

Liability insurance helps pay for injuries and property damage you cause to other people in an accident. Collision insurance helps pay for damage to your vehicle after a covered collision accident, regardless of fault. Comprehensive insurance helps pay for repairs involving non-collision events such as theft, vandalism, hail, fire, or falling objects.

This combination is why many people refer to it as full coverage car insurance when researching their options. It offers protection for both your financial responsibility to others and your own vehicle. For drivers with financed or leased vehicles, lenders often require comprehensive and collision coverage because they have a financial interest in the vehicle. The added protection helps reduce financial risk if the vehicle is damaged or totaled.

To learn more about available auto insurance options, it's important to compare different coverage levels and determine which coverage best fits your situation.

Get A Quote Now

What does full coverage car insurance cover?

One of the most important questions drivers ask is: what does full coverage car insurance cover? Although coverage varies by insurer and policy limits, full coverage typically includes coverage for several common situations.

Liability coverage

Liability insurance may help pay for:

- Medical expenses for injured third parties

- Property damage to another person's vehicle

- Legal expenses related to covered claims

Collision coverage

Collision insurance may help cover damage to your vehicle resulting from:

- Accidents with another vehicle

- Single-vehicle accidents

- Collisions with objects such as guardrails or poles

Comprehensive coverage

Comprehensive insurance may help cover:

- Theft

- Vandalism

- Fire

- Hail damage

- Flooding

- Falling objects

- Animal-related damage

For example, if a tree branch falls on your parked vehicle during a storm, comprehensive coverage may help pay for repairs. If you accidentally back into a pole in a parking lot, collision coverage may apply. Understanding what full coverage car insurance covers helps drivers see how multiple coverages work together to protect against a wide variety of risks.

However, full coverage does not cover everything. Common exclusions may include routine maintenance, mechanical breakdowns, intentional damage, and certain custom vehicle modifications unless specifically added to your policy.

Is comprehensive insurance full coverage?

A common misconception is that comprehensive insurance alone qualifies as full coverage. The answer is no.

Comprehensive insurance is only one component of a full coverage policy. While comprehensive coverage helps to insure your vehicle against events such as theft, vandalism, fire, hail, and falling objects, it does not cover collision-related damage.

For example, if your car is stolen, comprehensive coverage may help pay for the loss. However, if you collide with another vehicle, comprehensive insurance will not cover that damage. Collision coverage would be needed instead.

Likewise, liability insurance remains necessary to cover injuries and property damage you cause to others. This is why comprehensive, collision, and liability insurance are commonly bundled together when discussing what full coverage car insurance is. Each coverage serves a different purpose, and together they create broader protection.

Liability versus full coverage insurance

When comparing insurance options, understanding the difference between liability-only insurance and full coverage is essential. Liability insurance focuses on protecting others when you are at fault for an accident. It does not typically pay for damage to your own vehicle.

Full coverage insurance adds protection for your vehicle through comprehensive and collision coverage.

Liability-only insurance

- Lower monthly premiums

- Covers injuries and property damage to others

- Does not protect your vehicle

Full coverage insurance

- Higher premiums

- Covers liability obligations

- Helps pay for damage to your car under the designated collision or comprehensive coverages

The choice often depends on how much financial risk you are willing to assume. If your vehicle is newer or has significant value, paying for repairs or replacement out of pocket may be difficult. In those cases, full coverage may provide greater peace of mind.

When evaluating minimum coverage versus full coverage, consider what you could realistically afford to lose if your vehicle were damaged or totaled.

What affects the cost of full coverage insurance?

Because full coverage includes additional protection, it generally costs more than liability-only insurance. Several factors influence pricing, such as:

Vehicle value

More expensive vehicles often cost more to insure because repair and replacement costs are higher.

Driving history

Drivers with accidents, tickets, or previous claims may pay higher premiums because insurers view them as higher risk.

Deductibles

Your deductible directly impacts your premium. A higher deductible may lower your monthly payment, while a lower deductible may increase it. Understanding car insurance deductibles can help you find the right balance between affordability and out-of-pocket costs.

Location

Where you live can affect pricing due to factors such as traffic density, theft rates, weather risks, and local claim trends.

Claims history

Frequent insurance claims can increase premiums because they may indicate a greater likelihood of future claims.

While full coverage costs more, the additional premium often reflects the broader financial protection provided.

When is full coverage insurance worth it?

Deciding whether full coverage is worth the cost depends on your vehicle, finances, and personal comfort with risk.

Newer vehicles

Newer vehicles typically benefit the most from full coverage because repair and replacement costs can be substantial.

Financed or leased vehicles

Lenders and leasing companies frequently require comprehensive and collision coverage throughout the life of the loan or lease.

Older vehicles

For older vehicles with lower market value, the cost of comprehensive and collision coverage may eventually outweigh the potential insurance payout.

Risk tolerance

Every driver has a different comfort level with financial risk. Some drivers prefer lower premiums and accept greater out-of-pocket exposure. Others value the protection and predictability that full coverage can provide.

Do I need GAP insurance if I have full coverage?

Many drivers ask if GAP insurance is needed if they already have full coverage. Possibly.

Full coverage and gap insurance serve different purposes. Full coverage generally pays the vehicle's current market value if it is totaled. GAP insurance helps cover the difference between the insurance payout and the amount still owed on a loan or lease.

If you owe more than your vehicle is worth, gap insurance may provide valuable additional protection.

Why choose Infinity Insurance Agency (IIA) for full coverage insurance

Finding the right coverage should not feel complicated. IIA helps drivers compare coverage options, identify available discounts, and understand how different policy choices affect both protection and cost.

Whether you are purchasing insurance for a newly financed vehicle or reviewing your current policy, IIA offers flexible options designed to fit different budgets and driving needs. The goal is simple: to help drivers make informed decisions without unnecessary pressure or confusion.

By comparing multiple coverage options, you can better understand what fits your vehicle, financial situation, and long-term goals, and an IIA agent can help you with this.

Get A Quote Now

Frequently asked questions (FAQs)

Does full coverage cover a stolen car?

Typically, yes, if you carry comprehensive coverage. Comprehensive coverage is the part of a full coverage policy that helps pay for theft, subject to your deductible.

Does full coverage pay if my car is totaled?

It can. Collision and comprehensive coverage may pay your vehicle's actual cash value, minus your deductible, if it is declared a total loss in the event of a covered loss.

Does full coverage cover someone else driving my car?

Often yes, if you gave them permission to drive. Coverage usually follows the vehicle rather than the driver, but it is subject to your policy terms like excluded drivers, so confirm with your agent before you hand over your keys to someone who is not listed on your policy.

Does full coverage include GAP insurance?

No. GAP insurance covers the difference between what you owe on a loan or lease, and the actual cash value of your car. GAP insurance is typically a separate add-on.

Does full coverage cover hail, flooding, or hitting an animal?

Yes, these are typically covered under comprehensive coverage, which handles non-collision events such as weather damage and animal strikes, subject to your deductible.

Does full coverage extend to a rental car while mine is being repaired?

It depends on the coverage and terms of your auto insurance policy. If your vehicle is being repaired after a covered collision or comprehensive claim, your policy may extend the same coverage to a rental car used as a temporary replacement while your vehicle is out of service. However, not all policies provide the same protection. Some policies only cover specifically listed vehicles or may have different rules for vacation or recreational rentals. Always review your policy or contact your insurance agent before driving a rental car, so you understand exactly what is and isn't covered.

Get the right full coverage insurance for your needs

Choosing the right insurance coverage involves balancing protection, cost, and risk. Understanding what full coverage insurance is can help you avoid unexpected coverage gaps and make more confident decisions about your financial protection.

Before purchasing a policy, take time to compare auto insurance quotes and review the coverage that matters most to you. If you have questions about your options, you can also speak with an insurance agent for personalized guidance. The right policy should match your vehicle, budget, and comfort level while providing the protection you need on the road.

Call for a Quote Today