About 3 million businesses call Texas home, making it one of the world’s biggest economies. Having commercial auto insurance in Texas is essential to help with the high costs that can arise after a covered accident.

From landscaping businesses and HVAC contractors to food trucks and more, Infinity Insurance Agency, Inc. (IIA) helps small businesses looking for cheap commercial auto insurance in Texas. IIA offers:

- Discounts for qualifying drivers

- Same-day certificates of insurance (COIs) available

- Help from licensed, Spanish-bilingual agents

- Foreign driver’s licenses accepted

- Flexible payment options

- Automatic coverage for eligible, new-hire employees (depending on the insurer)

- Coverage options for cars/vans, trucks, and small fleets

Compare affordable commercial auto insurance options in Texas in minutes. Call us at 1-855-478-3705 or use our free commercial auto insurance calculator for an estimate.

What is commercial auto insurance?

Commercial auto insurance is a policy that can help pay for certain damages or injuries to you or someone else while you’re driving a business vehicle. This type of insurance can often go beyond personal auto insurance by addressing the unique risks small businesses face. Commercial auto insurance is required in most states.

Depending on your policy, this insurance may cover medical expenses, property damage, and legal fees after your business vehicle is involved in a covered accident.

To purchase it, you can contact one of our licensed, Spanish-bilingual agents. Or in Spanish: Visita la página de seguro de auto comercial en Texas.

Who needs commercial auto insurance in Texas?

If you drive a business vehicle to transport goods, get to a contracting site, deliver food, etc., you most likely need business auto insurance. IIA helps a variety of businesses find coverage, including:

- Trucking/transportation: Companies that transport goods, food, or equipment.

- Cleaning services: Small businesses that often drive to clients’ homes.

- Handyman businesses: Often transport equipment to client sites.

- Construction and contractors: These businesses often use vehicles to haul materials and tools.

- Food trucks: These businesses drive to different sites or events.

- Landscaping/lawncare: Vehicles used for landscaping or gardening services.

- Plumbing: Plumbers often use cars to transport equipment and visit clients.

- Electrical: Like plumbers, electricians commonly drive to client sites.

- HVAC contractors: Heating and cooling technicians often use vehicles for work-related tasks like site visits.

Don’t see your business listed? IIA offers budget-friendly commercial auto insurance options for a variety of enterprises in the Lone Star State. Call us today to get a free quote at 1-855-478-3705.

IIA coverage options for businesses in Texas

Every business is unique, which also means that your insurance policy may need a combination of coverages. At IIA, we offer a variety of coverage options, including:

- Liability coverage: This can help pay for bodily injury and vehicle damage to another driver’s vehicle if you’re at fault.

- General liability coverage: It may pay for damages or injuries sustained by non-employees at your business facility or caused by your business. This insurance can also help pay for medical and legal fees.

- Collision coverage: This can help cover damage to your vehicle after an accident, regardless of fault.

- Comprehensive coverage: This coverage may help pay for damages to your vehicle from non-collision incidents, such as theft or vandalism.

- Uninsured/underinsured motorist coverage: This can help cover damage to your vehicle or injuries you sustain from a driver who doesn’t have or lacks sufficient insurance.

Which business vehicles can be covered?

Whether you’re looking for commercial van insurance in Texas or coverage for your truck, IIA can help you find an option. Examples of vehicles that can be covered include:

- Pickup trucks

- Straight box trucks

- Flatbeds

- Dump trucks

- Vans

- Vehicles with attached equipment such as ladders or carpet washers

- Trailers, and more!

To get a commercial auto insurance quote in Texas, call one of our Spanish-bilingual agents at 1-855-478-3705 or get a free estimate online.

Texas commercial auto insurance requirements

In Texas, the state minimum requirement for personal auto insurance and commercial auto insurance is:

- $30,000 for bodily injury liability per person

- $60,000 for bodily injury liability for more than one person

- $25,000 for property damage per accident

Though these minimum requirements are helpful, they may not meet your business’s coverage needs. Depending on your business operations and risk exposure, you might want to consider additional coverage or purchasing higher liability limits.

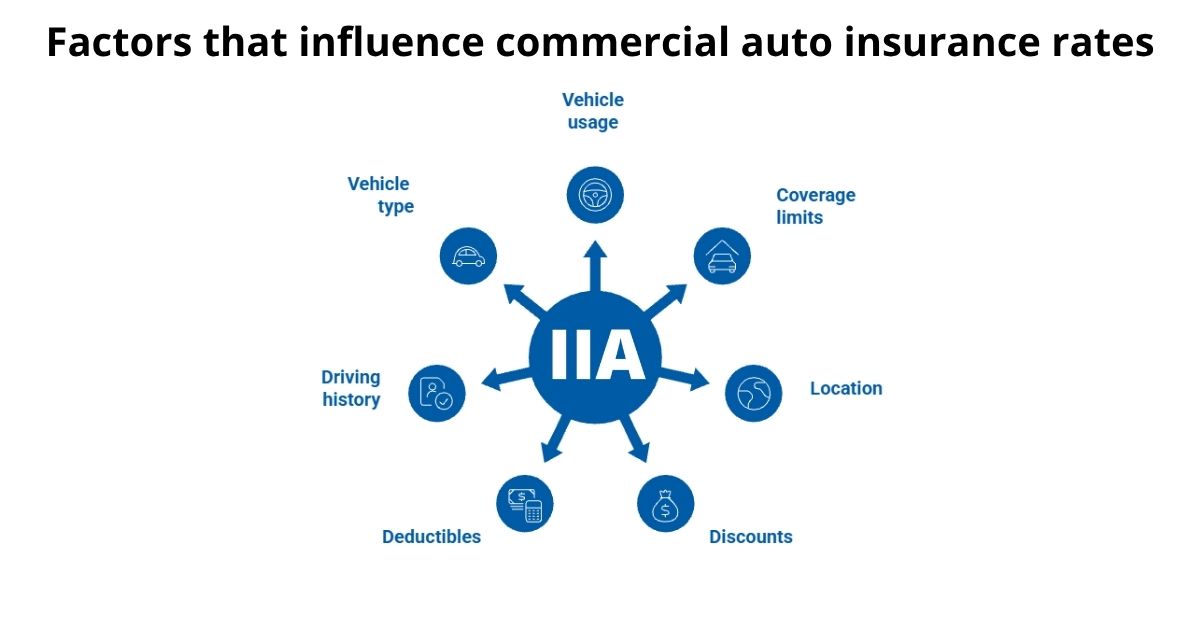

How much does commercial auto insurance cost in Texas?

The cost of commercial auto insurance can vary widely based on several factors, including:

- Type of business: Different industries have varying risk levels, which may impact insurance costs.

- Vehicle: Certain vehicles, like heavy-duty trucks or EVs, may cost more to insure.

- Driving records: The driving history of you and your employees may also be considered. A clean record may help lower your rates.

- Coverage amounts: Choosing higher coverage limits or purchasing additional coverage may increase your premium.

- Location: Where you’re located in the state, like whether your business is in an urban or rural area, may impact your insurance rates.

Save more with discounts

IIA works with major insurance companies that offer discounts for qualifying small businesses looking for cheap commercial auto insurance in Texas. These include:

- Discounts for bundling multiple vehicles

- Discounts for drivers who enroll in approved defensive driving courses

- Lower rates for paying your premiums in full

- Discounts for having previous car insurance coverage

- And more!

Ask one of our agents how you could save on auto insurance for your small business.

How it works

To get started with business auto insurance in Texas, you can follow these simple steps:

- Have your business and vehicle details ready to share with an IIA agent

- Compare affordable coverage options from 20+ insurance companies

- Build a customized policy and get same-day insurance ID cards or certificates of insurance (COIs) once your policy is active

Why Choose IIA?

Here’s how IIA stands out:

- Competitive rate options

- Discounts for qualifying drivers

- Same-day certificates of insurance (COIs) available

- Help from licensed, Spanish-bilingual agents

- Foreign driver’s licenses accepted

- Flexible payment options

- Help for “non-standard” drivers with previous insurance challenges

- Coverage options for cars/vans, trucks, and small fleets

Community engagement: We’ve partnered with the Rio Grande Hispanic Chamber of Commerce to support local businesses.

No matter where you are in Texas, you can purchase commercial auto insurance through Infinity Insurance Agency, Inc. Our reach extends from large cities to small towns, including:

- San Antonio

- Laredo

- Arlington

- El Paso

- Austin

- McAllen

- Pharr

- Lubbock

- Amarillo

- Fort Worth

- Corpus Christi

Ready to purchase quality insurance for your business? Call IIA today at 1-855-478-3705 or use our insurance calculator to get an estimate.